Table of Contents

What is Cash?

Cash is the money that a firm can disburse immediately without any restriction. In cash management, the term cash is used in both narrow and broad senses. In the narrow sense, it includes coins, currency, cheques, drafts held by the firm, and demand deposits in its bank accounts.

In the broader sense, it also covers near cash assets, i.e. marketable securities and time deposits in banks and other financial institutions. The word ‘cash management’ is, generally used for cash and near cash assets i.e. for both types of assets.

Without monitoring your cash how to measure it, invest it, borrow it, and collect it you can cheat yourself out of extra profits or even avoid trouble with creditors and bankruptcy. The main objective of cash management is an optimal cash balance; minimizing the sum of the fixed cost of transactions and the opportunity cost of holding cash balance.

Optimal balance here means a position when the cash balance amount is in the most ideal proportion so that the company has the ability to invest the excess cash for a return [profit] and at the same time have sufficient liquidity for future needs. The key ingredient here is that the cash balance should neither be excessive nor deficient.

For example, companies with many bank accounts may be accumulating excessive balances. Do you know how much cash you need, how much you have, where the cash is, what the sources of cash are, and where the cash will be used? This is especially crucial in a recession.

Meaning of Cash

The term “Cash” with reference to the management of cash is used in two ways. In a narrow sense, cash refers to coins, currency, cheques, drafts and deposits in banks. The broader view of cash includes near-cash assets such as marketable securities and time deposits in banks.

The reason why these near-cash assets are included in cash is that they can readily be converted into cash. Usually, excess cash is invested in marketable securities as it contributes to profitability. Cash is one of the most important components of current assets. Every firm should have adequate cash, neither more nor less.

Inadequate cash will lead to production interruptions, while excessive cash remains idle and will impair profitability. Any shortage of cash will hamper the operation of a concern and any excess of it will be unproductive. Cash is the most unproductive of all the assets.

While fixed assets like machinery, plant, etc., and current assets such as inventory will help the business in increasing its earning capacity, cash in hand will not add anything to the concern. Thus, cash is the balancing figure between debtors, stock, and creditors, without adequate cash to meet working capital demands, it is impossible to extend credit, order stock or pay creditors.

Nature of Cash

Cash is the money that a firm can disburse immediately without any restriction. In cash management, the term cash is used in both narrow and broad senses. In the narrow sense, it includes coins, currency, cheques, drafts held by the firm and demand deposits in its bank accounts.

In the broader sense, it also covers near cash assets, i.e. marketable securities and time deposits in banks and other financial institutions. The word ‘cash management’ is generally used for cash and near cash assets i.e. for both types of assets.

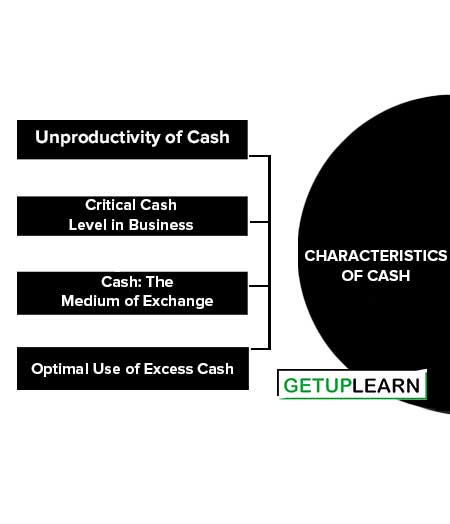

Characteristics of Cash

The following are the characteristics of cash:

- Unproductivity of Cash

- Critical Cash Level in Business

- Cash: The Medium of Exchange

- Optimal Use of Excess Cash

Unproductivity of Cash

Cash itself does not produce goods or services. Interest can be earned by depositing or lending it but it does not earn any profit like other assets. So it is called an unproductive asset. A shortage of cash is likely to harm the operations of a firm.

Critical Cash Level in Business

Every business needs to show a minimum of cash to carry out its business activities. If a business does not show sufficient cash balance, it will not be able to pay its creditors on time. This may be called a critical level of cash.

Cash: The Medium of Exchange

Cash is a medium of exchange and plays an important role as most of the transactions involve the flow of cash funds.

Optimal Use of Excess Cash

Deploying extra funds always involves opportunity costs. Therefore, excess cash should be invested in a profitable way to yield something in the form of interest and dividends rather than remaining idle.

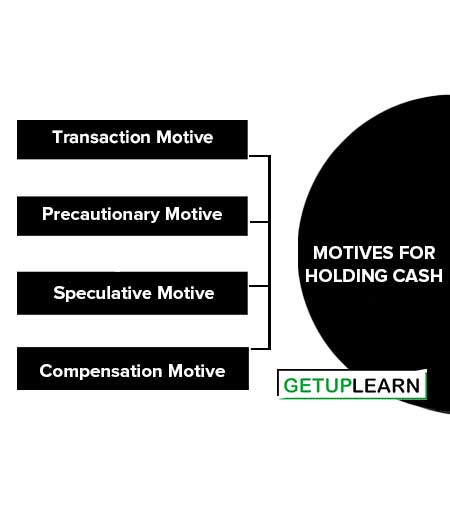

Motives for Holding Cash

Cash, the most liquid asset, is of vital importance to the daily operations of business firms. While the proportion of corporate assets held in the form of cash is very small, often between 1 and 4 percent, its efficient management is crucial to the solvency of the business because in a very important sense cash is the focal point of fund flows in a business.

In view of its importance, it is generally referred to as the “lifeblood of a business enterprise.” Why does a firm need cash? As John Maynard Keynes put forth, the following are the possible motives for holding cash:

Transaction Motive

A firm needs cash for making transactions in day-to-day operations. The cash is needed to make purchases, pay expenses, taxes, dividends, etc. The cash needs arise due to the fact that there is no complete synchronization between cash receipts and payments.

But the cash inflows and cash outflows do not perfectly synchronize. Sometimes, cash receipts are more than payments while at other times payments exceed receipts. The firm must have to maintain a sufficient (funds) cash balance if the payments are more than receipts.

Thus, the transaction motive refers to the holding of cash to meet expected obligations whose timing is not perfectly matched with cash receipts. Though a large portion of cash held for transactions motive is in the form of cash, a part of it may be invested in marketable securities whose maturity conforms to the timing of expected payments such as dividends, taxes, etc.

Precautionary Motive

A firm is required to keep cash for meeting various contingencies. Though cash inflows and cash outflows are anticipated there may be variations in these estimates. For example, a debtor who was to pay after 7 days may inform of his inability to pay; on the other hand, a supplier who used to give credit for 15 days may not have the stock to supply or he may not be in a position to give credit at present.

In these situations cash receipts will be less than expected and cash payments will be more as purchases may have to be made for cash instead of credit. Such contingencies often arise in a business. A firm should keep some cash for such contingencies or it should be in a position to raise finances in a short period.

The cash maintained for contingency needs is not productive or it remains idle. However, such cash may be invested in a short period or low- marketable securities which may provide cash as and when necessary.

Speculative Motive

The speculative motive relates to the holding of cash for investing in profitable opportunities as and when they arise. Such opportunities do not come in a regular manner. These opportunities cannot be scientifically predicted but only speculation can be made about their occurrence.

For Example, the prices of shares and securities may be low at a time with an expectation that these will go up shortly. The prices of raw materials may fall temporarily and a firm may like to make purchases at these prices. Such opportunities can be availed of if a firm has a cash balance with it.

These transactions are speculative because prices may not move in the direction in which we suppose them to move. The primary motive of a firm is not to indulge in speculative transactions but such investment may be made at times.

Compensation Motive

This motive to hold cash balances is to compensate banks and other financial institutes for providing certain services and loans. Banks provide a variety of services to business firms like clearance of cheques, drafts, transfer of funds, etc. Banks charge a commission or fee for their services to the customers as indirect compensation.

Customers are required to maintain a minimum cash balance at the bank. This balance cannot be used for transaction purposes. Banks can utilize the balances to earn a return to compensate for their cost of services to the customers.

Such balances are compensating balances. These balances are also required by some loan agreements between a bank and its customers. Banks require a chest to maintain a minimum cash balance to compensate when the supply of credit is restricted and interest rates are rising.

Thus cash is required to fulfill the above motives. Out of the four motives for holding cash balances, transaction motives, and compensation motives are very important. Business firms usually do not speculate and need not have speculative balances. The requirement of precautionary balances can be met out of short-term borrowings.

Factors Determining Cash Needs

The amount of cash for transaction requirements is predictable and depends upon a variety of factors. The factors determining cash needs are explained below:

- Credit Position of the Firm

- Status of Firm Receivable

- Status of Firm Inventory Account

- Nature of Business Enterprise

- Management Attitude Towards Risk

- Amount of Sales in Relation to Assets

- Cash Inflows and Cash Outflows

- Cost of Cash Balance

Credit Position of the Firm

The credit position influences the amount of cash required in two distinct ways:

- If a firm’s credit position is sound, it is not necessary to carry a large cash reserve for emergencies.

- If a firm finances its inventory requirements with trade credit, its cash requirements are considerably smaller, since the firm can synchronize the credit terms it gives to its customers with the terms it receives.

Status of Firm Receivable

The amount of time required for a firm to convert its receivable into cash also affects the amount of cash needed and of course, reduces the total working capital employed.

In other words, the longer the credit terms, the slower the turnover. When flow out is not synchronized with turnover, the firm must carry amounts of cash relatively larger than would otherwise be required.

Status of Firm Inventory Account

The status of a firm’s inventory account also affects the amount of cash tied up at any one time. For example, if one business firm carries two months of inventory on hand and another firm carries only one month’s supply, the former has twice as much investment in inventory and will normally be called upon to maintain a larger investment in cash in order to finance its acquisition.

Nature of Business Enterprise

The nature of a firm’s demand definitely affects the volume of cash required. For example, a firm whose demand is volatile needs a relatively larger cash reserve than one whose demand is stable. Public utility firms exhibit stable demand whereas firms that deal with high fashion merchandise or goods that tend to be “faddish” are subject to high degrees of volatility.

Management Attitude Towards Risk

More conservative management will hold a larger cash reserve than one that is less conservative. The former usually demands more liquidity than the latter and consequently does not experience the same degree of efficiency.

A generalization is made that the firm that effectively plans policies is less conservative than the one that does little or no planning. The obvious conclusion is that planning allows the firm to predict its requirements more accurately, thereby eliminating uncertainty, which is the basis for large cash reserves.

Amount of Sales in Relation to Assets

Another characteristic affecting the level of cash is the amount of sales in relation to assets. Firms with large sales relative to fixed assets are required to carry larger cash reserves. This is the result of having larger sums invested in inventories (particularly finished goods) and receivables.

It should be remembered, however, that cash requirements do not increase in the same proportion as sales. The rule is that as sales increase, cash also increases but at a decreasing rate, it is impossible to determine to what extent each characteristic affects the total volume of cash, but these examples indicate that different types of businesses have different cash requirements.

Cash Inflows and Cash Outflows

Every firm has to maintain cash balance because it’s expected and outflows are not always synchronized. The timing of the cash inflows may not always match with the timing of the outflows. Therefore, a cash balance is required to fill up the gap arising out of differences in timings and quantum of inflows and outflows.

Cost of Cash Balance

Another factor to be considered while determining the minimum cash balance is the cost of maintaining excess cash or meeting shortages of cash. There is always an opportunity cost of maintaining an excessive cash balance. If a firm is maintaining excess cash then it is missing the opportunities of investing these funds in a profitable way.

Cash Budget

A cash Budget is a planning tool in the hands of the management of a business organization. As we have discussed earlier, the objective of cash management is to ensure that the firm has an optimum balance of cash only i.e. neither the firm has an excess cash balance nor a shortage of cash at any stage.

A cash budget is a statement of estimated cash inflows and cash expenditure over the firm’s planning horizon and it helps the business organization in the identification of periods when there will be excess cash and also those periods when there will be a shortage of cash. After the identification of cash surplus and cash shortage periods firm will be in a better position to do the appropriate planning for cash.

The objectives of preparing the cash budget are:

- To identify the period when there is likely to be a shortage of cash.

- To identify the period when there is likely to be excess cash.

- To enable the firm to do proper planning for the procurement of cash at the least possible cost during the periods when there is a shortage of cash.

- To enable the firm to do proper planning for the investment of cash at the highest possible rate of return when there is a surplus of cash

With advance planning through a cash budget, firms get adequate time to take the necessary action for borrowing and lending cash on the terms most advantageous to it.

Process of Preparing Cash Budget

These are the steps of the process of preparing cash budget:

Planning Period

The first step in the process of preparation of the cash budget is the selection of the period to be covered by the cash budget and also the sub-periods within that time span over which the cash flows are to be projected. There is no fixed rule for this legally or even otherwise.

The planning period to be covered varies from firm to firm depending upon the business scale, nature of the business, credit policy, and degree of uncertainty involved in the business.

The higher the degree of certainty in a business, the longer can be the horizon of the cash budget and vice-versa. In the case of organizations facing extreme degrees of fluctuations, a cash budget can be prepared even on a daily basis.

Consideration of Factors having a bearing on Cash Budget

The second step in the process of preparation of a cash budget is the identification of the factors affecting cash estimation and the magnitude of their effect on the cash positions. For the purpose of preparation of cash budget, cash receipts, and cash payments can be classified into two categories i.e. Operating and Financial.

Operating cash flows are the cash flows associated with the operations of the firm while financial cash flows include cash flows that have resulted from sources other than the operations of the business.

Examples of operating cash flows include receipts from sales, collections from debtors, Payments to suppliers, administrative and selling expenses, etc.

Examples of financial cash flows include loans and Borrowings, interest received, Dividend received, interest paid, the dividend paid, etc. After the decision is taken about the span of the cash budget and also the factors to be considered in preparing the cash budget, one can move ahead and start preparing the cash budget.

FAQs About the What is Cash?

What are the characteristics of cash?

Unproductivity of Cash, Critical Cash Level in Business, Cash: The Medium of Exchange, and Optimal Use of Excess Cash are the characteristics of cash.

What are the motives for holding cash?

The following are the motives for holding cash:

1. Transaction Motive

2. Precautionary Motive

3. Speculative Motive

4. Compensation Motive.

What factors determine the need for cash?

The amount of cash for transaction requirements is predictable and depends upon a variety of factors. The factors determining cash needs are explained below:

1. Credit Position of the Firm

2. Status of Firm Receivable

3. Status of Firm Inventory Account

4. Nature of Business Enterprise

5. Management Attitude Towards Risk

6. Amount of Sales in Relation to Assets

7. Cash Inflows and Cash Outflows

8. Cost of Cash Balance.