Table of Contents

What is Receivables?

Receivables mean the book debts or debtors and these arise if the goods are sold on credit which may be converted to cash after the credit period. Debtors form about 30% of current assets in India. Debt involves an element of risk and bad debts also.

Hence, it calls for careful analysis and proper management. The goal of receivables management is to maximize the value of the firm by achieving a tradeoff between risk and profitability. For this purpose, a finance manager has:

- To obtain the optimum (non-maximum) value of sales.

- To control the cost of receivables, cost of collection, administrative expenses, bad debts, and the opportunity cost of funds blocked in the receivables.

- To maintain the debtors at a minimum according to the credit policy offered to customers.

- To offer cash discounts suitably depending on the cost of receivables, bank rate of interest, and the opportunity cost of funds blocked in the receivables.

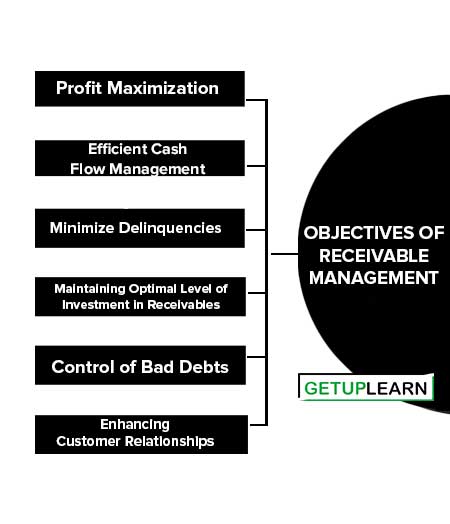

Objectives of Receivable Management

Accounts receivable management means managing the credit sales of the firm. The basic objective of accounts receivable management is to collect the funds due and to help the management in meeting their cash flow requirements. Effective accounts receivable management in achieving the desired cash flow through the timely collection of outstanding debts.

Objectives of receivable management are as follows:

- Profit Maximization

- Efficient Cash Flow Management

- Minimize Delinquencies

- Maintaining Optimal Level of Investment in Receivables

- Control of Bad Debts

- Enhancing Customer Relationships

Profit Maximization

The ultimate objective is to contribute to the maximization of the firm’s profit. This involves a balance between extending credit to increase sales and minimizing the cost of the bad debts that inevitably come with increased credit sales.

Efficient Cash Flow Management

By managing receivables effectively, the firm can ensure a healthy cash flow. This involves establishing effective credit policies and collection procedures to speed up collections and reduce the cash conversion cycle.

Minimize Delinquencies

One of the goals is to keep delinquencies (late payments) to a minimum. This involves credit checks and monitoring customer payments to identify any potential issues as early as possible.

Maintaining Optimal Level of Investment in Receivables

The objective is to maintain an optimal balance between receivables and sales. Too high an investment in receivables can lead to higher costs (such as opportunity cost of tied-up capital and bad debts), and too low an investment can lead to lost sales opportunities.

Control of Bad Debts

An important objective is to control the risk of bad debts, i.e., uncollectible accounts. This involves careful assessment of credit risk and setting appropriate credit terms and limits.

Enhancing Customer Relationships

Efficient receivable management also aims to maintain and enhance relationships with customers. It’s important to manage receivables without alienating or losing valuable customers.

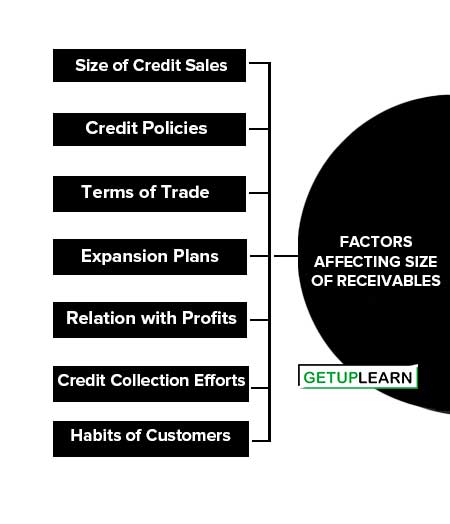

Factors Affecting Size of Receivables

Besides sales, a number of other factors also influence the size of receivables. The following factors, directly and indirectly, affect the size of receivables.

The size of accounts receivable is determined by a number of factors. Some of the important factors affecting size of receivables are:

- Size of Credit Sales

- Credit Policies

- Terms of Trade

- Expansion Plans

- Relation with Profits

- Credit Collection Efforts

- Habits of Customers

Size of Credit Sales

The volume of credit sales is the first factor that increases or decreases the size of receivables. If a concern sells only on a cash basis as in the case of Bata Shoe Company, then there will be no receivables. The higher the part of credit sales out of total sales, the figures of receivables will also be more, or vice versa.

Credit Policies

A firm with a conservative credit policy will have a low size of receivables while a firm with a liberal credit policy will be increasing this figure.

If collections are prompt then even if credit is liberally extended the size of receivables will remain under control. In case receivables remain outstanding for a longer period, there is always a possibility of bad debts.

Terms of Trade

The size of receivables also depends upon the terms of trade. The period of credit allowed and rates of discount given are linked with receivables.

If the credit period allowed is more then receivables will also be more. Sometimes trade policies of competitors have to be followed otherwise it becomes difficult to expand sales.

Expansion Plans

When a concern wants to expand its activities, it will have to enter new markets. To attract customers, it will give incentives in the form of credit facilities.

The period of credit can be reduced when the firm is able to get permanent customers. In the early stages of expansion, more credit becomes essential and the size of receivables will be more.

Relation with Profits

The credit policy is followed with a view to increasing sales. When sales increase beyond a certain level the additional costs incurred are less than the increase in revenues. It will be beneficial to increase sales beyond the point because it will bring more profits. The increase in profits will be followed by an increase in the size of receivables or vice-versa.

Credit Collection Efforts

The collection of credit should be streamlined. The customers should be sent periodical reminders if they fail to pay on time. On the other hand, if adequate attention is not paid to credit collection then the concern can land itself in a serious financial problem. An efficient credit collection machinery will reduce the size of receivables.

Habits of Customers

The paying habits of customers also have a bearing on the size of receivables. The customers may be in the habit of delaying payments even though they are financially sound. The concern should remain in touch with such customers and should make them realize the urgency of their needs.

Optimum Size of Receivables

The optimum investment in receivables will be at a level where there is a trade-off between costs and profitability. When the firm resorts to a liberal credit policy, the profitability of the firm increases on account of higher sales.

However, such a policy results in increased investment in receivables, increased chances of bad debts and more collection costs. The total investment in receivables increases and, thus, the problem of liquidity is created.

On the other hand, a stringent credit policy reduces profitability but increases the liquidity of the firm. Thus, optimum credit policy occurs at a point where there is a “Trade-off” between liquidity and profitability.

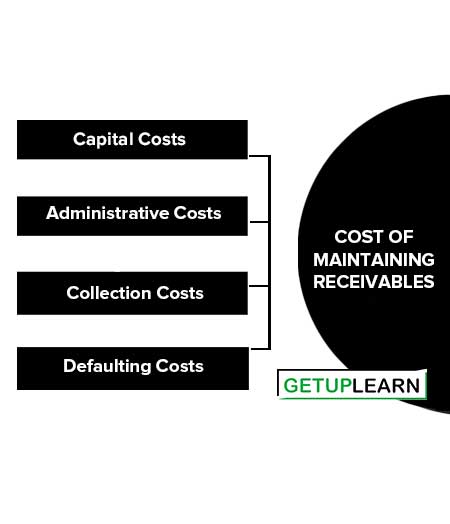

Cost of Maintaining Receivables

The cost of maintaining receivables, also known as the cost of carrying receivables, represents the expenses incurred by a company when offering credit to its customers. It’s an important factor to consider in the management of accounts receivable. Here are the main components of the cost of maintaining receivables:

Capital Costs

Maintenance of accounts receivable results in the blocking of the firm’s financial resources in them. This is because there is a time lag between the sale of goods to customers and the payments by them. The firm has, therefore, to arrange for additional funds to meet its own obligations, such as payment to employees, suppliers of raw materials, etc. while waiting for payments from its customers.

Additional funds may either be raised from outside or out of profits retained in the business. In first the case, the firm has to pay interest to the outsider while in the latter case, there is an opportunity cost to the firm, i.e., the money which the firm could have earned otherwise by investing the funds elsewhere.

Administrative Costs

The firm has to incur additional administrative costs for maintaining accounts receivable in the form of salaries to the staff kept for maintaining accounting records relating to customers, the cost of conducting investigations regarding potential credit customers to determine their creditworthiness, etc.

Collection Costs

The firm has to incur costs for collecting payments from its credit customers. Sometimes, additional steps may have to be taken to recover money from defaulting customers.

Defaulting Costs

Sometimes after making all serious efforts to collect money from defaulting customers, the firm may not be able to recover the over dues because of the inability of the customers. Such debts are treated as bad debts and have to be written off since they cannot be realized. Such debts are treated as bad debts and have to be written off since they cannot be realized.

Advantages of Receivable Management

These are the advantages of receivable management:

Increase in Sales

Except for a few monopolistic firms, most of the firms are required to sell goods on credit, either because of trade customers or other conditions. The sales can further be increased by liberalizing the credit terms. This will attract more customers to the firm resulting in higher sales and growth of the firm.

Increase in Profits

An increase in sales will help the firm (i) easily recover the fixed expenses and attain the break-even level, and (ii) increase the operating profit of the firm. In a normal situation, there is a positive relation between the sales volume and the profit.

Extra Profit

Sometimes, the firms make the credit sales at a price that is higher than the usual cash selling price. This brings an opportunity for the firm to make an extra profit over and above the normal profit.

To Face Competition

The firm may efficiently face the challenges posed by competitors.

FAQs About the Receivables

What are the objectives of receivable management?

The following are the objectives of receivable management:

1. Profit Maximization

2. Efficient Cash Flow Management

3. Minimize Delinquencies

4. Maintaining an Optimal Level of Investment in Receivables

5. Control of Bad Debts

6. Enhancing Customer Relationships.

What are the factors affecting size of receivables?

The following are the factors affecting size of receivables:

1. Level of credit sales

2. Credit Policies

3. Terms of Trade.

What is the cost of maintaining receivables?

The following are the components of cost of maintaining receivables:

1. Capital Costs

2. Administrative Costs

3. Collection Costs

4. Defaulting Costs.

What are the advantages of receivable management?

The advantages of receivable management are:

1. Increase in Sales

2. Increase in Profits

3. Extra Profit

4. To Face Competition.

What are the factors affecting the size of receivables?

The following are the factors affecting the size of receivables:

1. Size of Credit Sales

2. Credit Policies

3. Terms of Trade

4. Expansion Plans

5. Relation with Profits

6. Credit Collection Efforts

7. Habits of Customers.