Table of Contents

What is Commercial Bank?

The term “commercial bank” can be defined as a financial institution that accepts deposits, offers checking account services, make various loans, and offers basic financial products like certificates of deposit (CDs) and savings accounts to individuals and small businesses.

A commercial bank is where most people do their banking. Commercial banks make money by providing and earning interest from loans such as mortgages, auto loans, business loans, and personal loans. Customer deposits provide banks with the capital to make these loans.

These banks perform all kinds of banking business and generally finance trade and commerce. Their deposits are for a short period. These banks normally advance short-term loans to businessmen and traders and avoid medium-term and long-term lending.

However, commercial banks have extended their areas of operations to medium-term and long-term finance. The majority of the commercial banks are in the public sector. But there are certain private sector banks operating as joint stock companies. Hence, commercial banks are also called joint-stock banks.

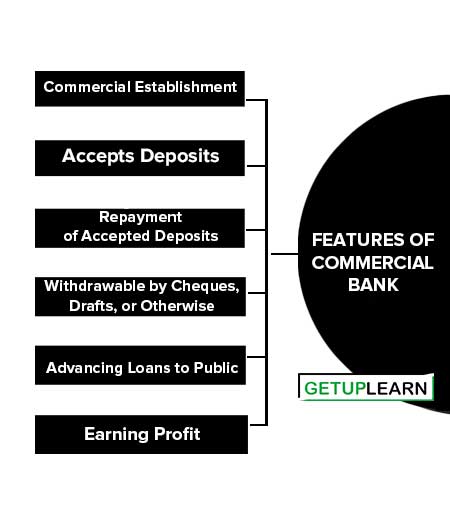

Features of Commercial Bank

The following are the important features of commercial bank:

- Commercial Establishment

- Accepts Deposits

- Repayment of Accepted Deposits

- Withdrawable by Cheques, Drafts, or Otherwise

- Advancing Loans to Public

- Earning Profit

Commercial Establishment

A commercial bank is a commercial establishment, which deals in debts and money.

Accepts Deposits

A bank accepts deposits from the public. People can deposit their cash balances in either of the following accounts at their convenience:

- Fixed Deposit Account

- Current Deposit Account

- Savings Deposit Account

- Recurring Deposit Account, etc.

Repayment of Accepted Deposits

The bank repays the accepted deposits to the true owner when required by him on demand or otherwise. The customer has to make the demand for repayment of money to the bank.

Withdrawable by Cheques, Drafts, or Otherwise

The deposited money with a bank can be withdrawable through cheques, drafts, or otherwise during banking hours.

Advancing Loans to Public

The bank can lend some money not required by the true owner to those who are in need of money to earn interest. The public can borrow money from banks to meet their needs and requirements.

Earning Profit

Profit earning is the main aim of the bank as a commercial establishment. The profit of a bank is the difference between the rate of interest paid by the bank on deposited money and the rate of interest received by the bank on lending money. Thus, we can conclude that the banks borrow in order to lend. They borrow in the form of deposits from the public.

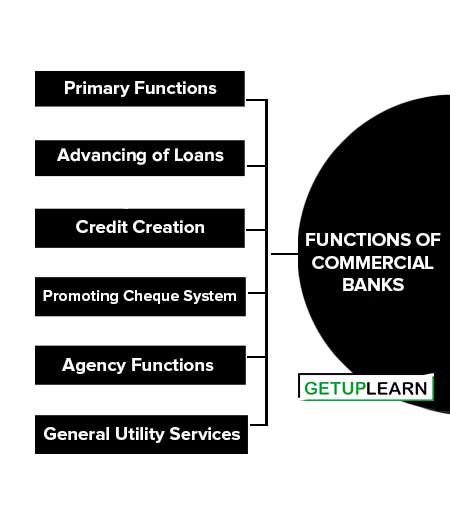

Functions of Commercial Banks

In The modern world, banks perform a variety of functions that it is not possible to list out all of their functions and services. However, some basic functions of commercial banks are discussed below:

- Primary Functions

- Advancing of Loans

- Credit Creation

- Promoting Cheque System

- Agency Functions

- General Utility Services

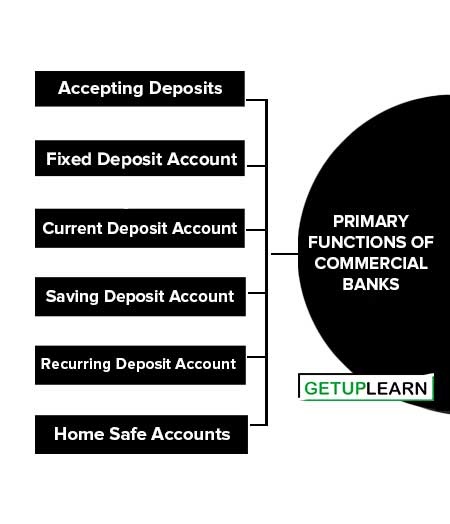

Primary Functions

These are the following primary functions of commercial banks:

- Accepting Deposits

- Fixed Deposit Account

- Current Deposit Account

- Saving Deposit Account

- Recurring Deposit Account

- Home Safe Accounts

Accepting Deposits

The first important function of a bank is to accept deposits from those who can save but cannot profitably utilize those saving by themselves.

People consider it more rational to deposit their savings in a bank because by doing so they earn interest on one hand and avoid the danger of theft on the other. To attract and promote savings from all sorts of individuals, banks maintain different types of accounts.

Fixed Deposit Account

In these accounts customer deposits money for a fixed period of time say one, two, or five years, etc, and cannot withdraw before the expiry of that period.

The rate of interest on this account is higher than that on other types of deposits. The longer the period, the higher will be the rate of interest. Fixed deposits are also called time deposits or time liabilities.

Current Deposit Account

These accounts are generally maintained by traders and businessmen who have to make a number of payments every day. Money can be withdrawn as many times and in as much amount as desired by the depositors.

Generally, no interest is paid on these accounts. And the deposits have to pay certain incidental charges to the bank for the services rendered by it. These are also called demand deposits or demand liabilities.

Saving Deposit Account

The aim of these accounts is to encourage and mobilize small savings of the public certain restrictions are imposed on the depositors regarding the number of withdrawals and the amount to be withdrawn in a given period.

A Cheque facility is provided to the depositors. The rate of interest paid on these deposits is low compared to that on fixed deposits.

Recurring Deposit Account

The purpose of these accounts is to encourage regular savings by the public, particularly by the fixed-income group. Generally, money in these accounts is deposited in monthly installments for a fixed period and is repaid to the depositors along with interest on maturity. The rate of interest on these deposits is nearly the same as on fixed deposits.

Home Safe Accounts

This scheme aims at promoting the saving habits of the people. Under the scheme, a safe is supplied to the depositor to keep at home and to put his small savings in it. Periodically, the safe is taken to the bank where the amount of the safe is credited to his account.

Advancing of Loans

The second important function of a bank is advancing loans to the public. After keeping certain cash reserves, the banks lend their deposits to needy borrowers. Before advancing loans, the banks satisfy themselves about the creditworthiness of the borrowers. Various types of loans granted by the banks are:

Money at Call

Such loans are very short-period loans and can be called back by the bank at a very short notice of say one day to fourteen days. These loans are given to other banks or financial institutions.

Cash Credit

It is a type of loan that is given to the borrower against his current assets, such as shares, stocks, bonds, etc. Such loans are not based on personal security.

The bank opens the account in the name of the borrower and allows him to withdraw borrowed money from time to time up to a certain limit as determined by the value of his current assets. Interest is charged not only on this amount actually withdrawn from the account.

Overdraft

The bank provides overdraft facilities to its customers in times of need i.e., customers are allowed to withdraw more than their deposits. Interest is charged to the customers from the overdrawn amount.

Discounting of Bills of Exchange

This is another type of lending by modern banks. Through this method, a holder of a bill of exchange can get it discounted by the bank. In a bill of exchange, the debtor accepts the bill drawn upon him by the creditor, who is the holder of the bill, and agrees to pay the amount mentioned on maturity.

After making some marginal deductions in the form of a commission, the bank pays the value of the bill to the holder. When the bill of exchange matures, the bank gets its payment from the party which had accepted the bill. Thus, such a loan is self-liquidating.

Term Loans

The banks have also started advancing medium-term and long-term loans. The maturity period for such loans is more than one year. The amount sanctioned is either paid or credited to the amount of the borrower. The interest is charged on the entire amount of the loan and the loan is repaid either on maturity or in installments.

Credit Creation

Credit creation is a unique function of the bank. Credit creation is the outcome of the process of advancing loans as adopted by the banks when a bank sanctions a loan t its customer, it does not lend cash but opens an account in the borrower’s name and credits the amount of the loan to that account.

Thus, whenever a bank grants a loan, it creates an equal amount of bank deposit. The creation of such deposits is called credit creation which results in an increase in the stock of money in the economy.

Banks have the ability to create credit many more times than their deposits and this ability of multiple credit creation depends upon the cash reserve ratio of the banks.

Promoting Cheque System

Banks provide a very useful medium of exchange in the form of cheques. Cheque is the most developed credit instrument in the money market.

Through a cheque, the depositor directs the banker to make payment of the cheque to the payee. In modern business transactions, cheques have become a much more convenient method of setting debts than the use of cash.

Agency Functions

Banks perform certain agency functions for and on behalf of their customers:

- Remittance of Funds

- Collection and Payment of Credit Instruments

- Execution of Standing Orders

- Purchasing and Sale of Securities

- Collection of Dividends on Shares

- Income Tax Consultancy

- Acting as Trustee and Executor

- Acting as Representative and Correspondent

Remittance of Funds

Banks help their customers in transferring funds from one place to another through cheques, drafts, etc.

Collection and Payment of Credit Instruments

Banks collect and pay various credit instruments like cheques, bills of exchange, promissory notes, etc.

Execution of Standing Orders

Banks execute the standing instructions of their customers for making various periodic payments. They pay subscriptions, rents, insurance premia, etc., on behalf of their customers.

Purchasing and Sale of Securities

Banks undertake the purchase and sale of various securities like shares, stocks, bonds, debentures, etc on behalf of their customers. Banks neither give any advice to their customers regarding these investments nor levy any charge on them for their service, but simply perform the function of a broker.

Banks collect dividends, interest on shares, and debentures of their customers.

Income Tax Consultancy

Banks appoint income tax experts to prepare income tax returns for their customers and to help them to get refunds of income tax.

Acting as Trustee and Executor

Banks preserve the wills of their customer’s ad execute them after their death.

Acting as Representative and Correspondent

Sometimes the banks act as representatives and correspondents of their customers. They get passports, and traveler’s tickets, book vehicles, and plots for their customers and receive letters on their behalf.

General Utility Services

In addition to agency services, modern banks provide many general utility services as given below:

- Locker Facility

- Traveler’s Cheques

- Letter of Credit

- Collection of Statistics

- Underwriting Securities

- Gift Cheques

- Acting as Referee

- Foreign Exchange Business

Locker Facility

Banks provide locker facilities to their customer. Customer can keep their valuables and important documents in the lockers for safe custody.

Traveler’s Cheques

Banks issue traveler’s cheques to help the customers to travel without the fear of theft or loss of money with this facility, the customers need not take the risk of carrying cash with them during their travels.

Letter of Credit

Banks issue letters of credit to their customers certifying their creditworthiness. Letters of credit are very useful in foreign trade.

Collection of Statistics

Banks collect statistics giving important information relating to industry, trade and Commerce, money, and banking. They also publish journals and bulletins containing research articles on economic and financial matters.

Underwriting Securities

Banks underwrite the securities issued by the government, public or private bodies. Because of its full faith in banks, the public will not hesitate in buying securities carrying the signatures of a bank.

Gift Cheques

Some banks issue cheques of various denominations (say of Rs.11,21,31,51,101, etc) to be used on auspicious occasions.

Acting as Referee

Banks may be referred for seeking information regarding the financial position, business reputation, and respectability of the customers.

Foreign Exchange Business

Banks also deal in the business of Foreign currencies. And they may finance foreign trade by rediscounting foreign bills of exchange.

Trends in Commercial Banking

After independence, the emergence of planning in the country has provided direction and purpose to commercial banks. A number of changes have taken place in the structure and functioning of the Indian banking system. Important among them are:

- Branch Expansion

- Deposit Mobilisation

- Credit Expansion

- Lead Bank Scheme

- Increase in Small Customers

- Development-Oriented Banking

- Regulation by Reserve Bank

- Advances to Priority Sectors

- Rural Development

- Innovative Banking

- Merchant Banking

Branch Expansion

A notable feature of the branch expansion has been a significant increase in the rural branches of the banks, particularly after the nationalization of major banks in 1969. There were 299 banks and their branches were 65,340 at the end of 2000. Nearly 60% of branches were scattered in rural areas.

Deposit Mobilisation

Commercial banks in India have played an important role in mobilizing deposits of the people. Total deposits of scheduled banks have increased from Rs.908 crore at the end of 1951. to Rs.8,10,070 crores at the end of 2000.

The deposits in rural areas have increased more rapidly than in urban and semi-urban areas. The increase in deposits has been mainly due to economic development deficit financing, increased currency, and expansion of banking facilities in the country.

Credit Expansion

The credit facility provided by commercial banks has been increasing significantly year after year. Total advances of the scheduled banks increased from Rs.547 crores in 1951 to Rs.3599 crore in 1969 and further to Rs.4,21,479 crores in 2000. Banks provided loan facilities, especially to agriculture, small-scale industries, and other priority sectors.

Lead Bank Scheme

The lead bank scheme was introduced by the Reserve Bank of India towards the end of 1969 with the objective of enabling commercial banks to assume the role of leadership for the development of banking and credit facilities throughout the country on the basis of an area approach.

Under this scheme, all the districts in the country have been allotted to the State Bank group, nationalized banks, and private Indian banks. A lead bank is assigned the role of a catalytic agent of economic development through the expansion of bank branches and diversification of credit facilities in the districts allotted to it.

The main objectives of a lead bank are:

- To open branches in all the important localities of lead districts.

- To expand maximum credit facilities for development in the district.

- To mobilize the savings of the people in the district.

- To co-ordinate the activities of cooperative banks commercial banks and other financial institutions in the district.

Increase in Small Customers

The banking services were shifted from big consumers to small customers. The banking system is becoming more and more popular among the common people of the country. About 60 percent of depositors of commercial banks are saving depositors mainly from low and middle-income groups.

Recently, there is a considerable increase in saving bank accounts also special schemes such as differential rate of interest schemes have been introduced in 1972 to provide concessional credit to economically and socially backward people to encourage productive activities. Nowadays banks show more concentration on financing small farmers, artisans, and small business firms.

Development-Oriented Banking

Initially, Indian banks were mainly concerned with the growth of commerce and some of the traditional industries such as cotton textiles and jute. The banks were concentrated in the big commercial centers and mostly short-term commercial loans were granted.

After independence, banking in India has adopted policies that are helpful for the development of the country. Now, the banks are providing medium-term and long-term loans and cater to the needs of the agricultural and industrial sectors.

Regulation by Reserve Bank

The Banking Regulation Act, of 1949 and its subsequent amendments have given adequate powers to the Reserve Bank of India to control and regulate the banking system of the country. Effective measures of the Reserve Bank have resulted:

- The protection of the interests of the depositors.

- Increase in public confidence in banks.

-

Controlling the frequent failures of the banks.

- Development of banks on sound lines and in the proper direction.

Advances to Priority Sectors

An important change after the nationalization of banks is the expansion of advances to the priority sectors. One of the objectives of the nationalization of banks was to extend credit to the borrowers of neglected sectors of the economy.

To achieve this objective, the banks formulated various schemes to provide credit to small borrowers in priority sectors like agriculture, small-scale business, transport, retail trade, etc. The total credit provided by the banks in 1969 was Rs.504 crores. It increased by Rs.1,35,923 crores in 2000. In 1969 the loans granted to priority sectors were 12% of the total loans and it was increased to 42% at the end of 2000.

Rural Development

Recently banks have recognized the social objectives and worked for rural development and for the removal of poverty. In 1978, the Government of India launched Integrated Rural Development Programme for removing imbalances in the rural economy and for the round progress of the rural areas.

Under this program, banks extended their services through various schemes. The program has shown notable progress in improving the standard of living of rural people.

Innovative Banking

Recently, Indian banks have introduced a number of innovations and diversifications in their operations to improve their performance. They are:

- Adopting a participatory approach.

- Adopting a consortium approach in lending.

- Provision of single-window lending.

- Introducing credit card facilities.

- Introducing new technology, mechanization, and computerization in lending operations.

- Entering into related activities such as merchant banking, mutual funds, hire-purchase finance, etc.

- Paying more attention to consolidation, sophistication, better consumer service, and greater profitability.

Merchant Banking

On account of their special knowledge of the financial needs of the traders, the merchant banks started the practice of accepting or guaranteeing the bills of exchange. The primary activity of merchant banks is providing financial services and guaranteeing sales and distribution of securities.

They handle all aspects of the sale of industrial securities i.e., their origination, underwriting, and distribution. They provide the services such as project promotion services, syndication of credit and other facilities project leasing, corporate advisory services, and management of and dealing in commercial papers.

In recent years, particularly after nationalization, commercial banking in India has been experiencing radical changes both quantitatively and qualitatively. The banking industry has grown geographically over the length and breadth of the country. The deposits and credit of the banks have multiplied.

The banks have also taken the new responsibilities of serving the national plans and priorities for economic development.

FAQs About the Commercial Bank

What are the functions of commercial banks?

The functions of commercial banks are:

1. Primary Functions: Accepting Deposits 2. Fixed Deposit Account 3. Current Deposit Account 4. Saving Deposit Account 5. Recurring Deposit Account 6. Home Safe Accounts

2. Advancing of Loans: Money at Call 2. Cash Credit 3. Overdraft

3. Credit Creation

4. Promoting Cheque System