Table of Contents

- 1 What is Negotiable Instruments Act 1881?

- 2 Characteristics of Negotiable Instruments

- 3 Presumption of Negotiable Instruments

- 4 Types of Negotiable Instruments

- 5 Difference Between Bills of Exchange and Cheques

- 6 Parties to Negotiable Instruments

- 7 Negotiation

- 8 FAQs About the Negotiable Instruments Act 1881

What is Negotiable Instruments Act 1881?

According to Section 13 (a) of the Act, “Negotiable instrument means a promissory note, bill of exchange or cheque payable either to order or to bearer, whether the word “order” or “ bearer” appears on the instrument or not.”

In the words of Justice, Willis, “A negotiable instrument is one, the property in which is acquired by anyone who takes it bonafide and for value notwithstanding any defects of the title in the person from whom he took it”.

Thus, the term, negotiable instrument means a written document that creates a right in favor of some person and which is freely transferable. Although the Act mentions only these three instruments (such as a promissory note, a bill of exchange, and a cheque), it does not exclude the possibility of adding any other instrument which satisfies the following two conditions of negotiability:

- The instrument should be freely transferable (by delivery or by indorsement. and delivery) by the custom of the trade.

- The person who obtains it in good faith and for value should get it free from all defects, and be entitled to recover the money of the instrument in his own name.

As such, documents like share warrants payable to the bearer, debentures payable to the bearer, and dividend warrants are negotiable instruments. But the money orders and postal orders, deposit receipts, share certificates, bills of lading, dock warrants, etc. are not negotiable instruments.

Although they are transferable by delivery and indorsements, they are not able to give a better title to the bonafide transferee for value than what the transferor has.

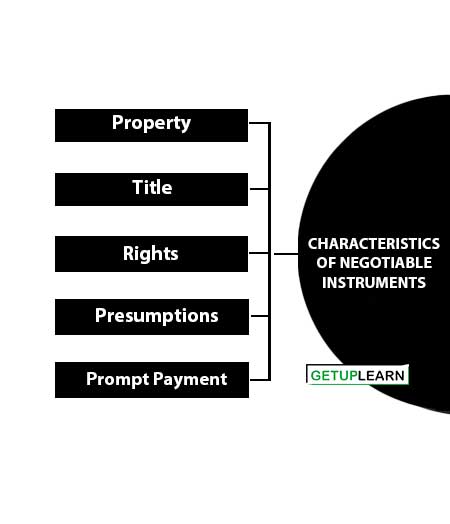

Characteristics of Negotiable Instruments

The following characteristics of negotiable instruments:

Property

The processor of the negotiable instrument is presumed to be the owner of the property contained therein. A negotiable instrument does not merely give possession of the instrument but right to property also. The property in a negotiable instrument can be transferred without any formality.

In the case of the bearer instrument, the property passes by mere delivery to the transferee. In the case of an order instrument, indorsement, and delivery are required for the transfer of property.

Title

The transferee of a negotiable instrument is known as the ‘holder in due course.’ A bona fide transferee for value is not affected by any defect of title on the part of the transferor or of any of the previous holders of the instrument.

Rights

The transferee of the negotiable instrument can sue in his own name, in case of dishonor. A negotiable instrument can be transferred any number of times till it is at maturity. The holder of the instrument need not give notice of transfer to the party liable for the instrument to pay.

Presumptions

Certain presumptions apply to all negotiable instruments e.g., a presumption that consideration has been paid under it. It is not necessary to write in a promissory note the words ‘for value received’ or similar expressions because the payment of consideration is presumed. The words are usually included to create additional evidence of consideration.

Prompt Payment

A negotiable instrument enables the holder to expect prompt payment because a dishonor means the ruin of the credit of all persons who are parties to the instrument.

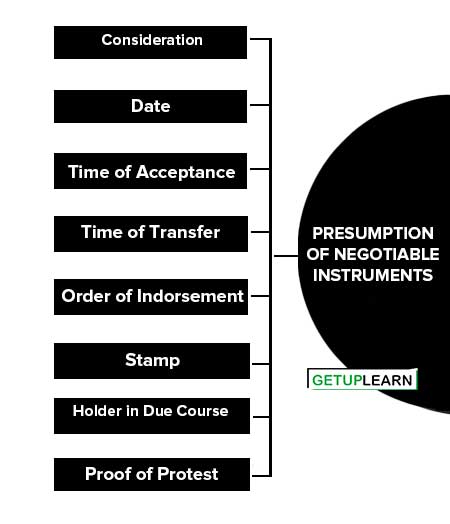

Presumption of Negotiable Instruments

Sections 118 and 119 of the Negotiable Instrument Act lay down certain presumptions that the court presumes in regard to negotiable instruments.

In other words, these presumptions need not be proved as they are presumed to exist in every negotiable instrument. Until the contrary is proved the following presumption of negotiable instruments:

- Consideration

- Date

- Time of Acceptance

- Time of Transfer

- Order of Indorsement

- Stamp

- Holder in Due Course

- Proof of Protest

Consideration

It shall be presumed that every negotiable instrument was made drawn, accepted, or endorsed for consideration.

It is presumed that consideration is present in every negotiable instrument until the contrary is presumed. The presumption of consideration, however, may be rebutted by proof that the instrument had been obtained from, its lawful owner by means of fraud or undue influence.

Date

Where a negotiable instrument is dated, the presumption is that it has been made or drawn on such date, unless the contrary is proved.

Time of Acceptance

Unless the contrary is proved, every accepted bill of exchange is presumed to have been accepted within a reasonable time after its issue and before its maturity. This presumption only applies when the acceptance is not dated; if the acceptance bears a date, it will prima facie be taken as evidence of the date on which it was made.

Time of Transfer

Unless the contrary is presumed it shall be presumed that every transfer of a negotiable instrument was made before its maturity.

Order of Indorsement

Until the contrary is proved it shall be presumed that the indorsements appearing upon a negotiable instrument were made in the order in which they appear thereon.

Stamp

Unless the contrary is proved, it shall be presumed that a lost promissory note, bill of exchange or cheque was duly stamped.

Holder in Due Course

Until the contrary is proved, it shall be presumed that the holder of a negotiable instrument is the holder in due course.

Every holder of a negotiable instrument is presumed to have paid consideration for it and to have taken it in good faith. But if the instrument was obtained from its lawful owner by means of an offense or fraud, the holder has to prove that he is a holder in due course.

Proof of Protest

Section 119 lays down that in a suit upon an instrument that has been dishonored, the court shall on proof of the protest, presume the fact of dishonor, unless and until such fact is disproved.

Types of Negotiable Instruments

Section 13 of the Negotiable Instruments Act states that a negotiable instrument is a promissory note, bill of exchange, or cheque payable either to order or to bearer. This list of negotiable instruments is not a closed chapter.

With the growth of commerce, new kinds of securities may claim recognition as negotiable instruments. The courts in India usually follow the practice of English courts according to the character of negotiability to other instruments. The types of negotiable instruments are explained below:

Promissory Notes

Section 4 of the Act defines, “A promissory note is an instrument in writing (note being a bank-note or a currency note) containing an unconditional undertaking, signed by the maker, to pay a certain sum of money to or to the order of a certain person, or to the bearer of the instruments.”

Essential Elements: An instrument to be a promissory note must possess the following elements:

- It must be in writing: A mere verbal promise to pay is not a promissory note. The method of writing (either in ink or pencil or printing, etc.) is unimportant, but it must be in any form that cannot be altered easily.

- It must certainly be an express promise or clear understanding to pay: There must be an express undertaking to pay. A mere acknowledgment is not enough. The following are not promissory notes as there is no promise to pay.

Bill of Exchange

Section 5 of the Act defines, “A bill of exchange is an instrument in writing containing an unconditional order, signed by the maker, directing a certain person to pay a certain sum of money only to, or to the order of a certain person or to the bearer of the instrument”.

A bill of exchange, therefore, is a written acknowledgment of the debt, written by the creditor and accepted by the debtor. There are usually three parties to a bill of exchange drawer, the acceptor or drawee and the payee. The drawer himself may be the payee.

Essential conditions of a bill of exchange:

- It must be in writing.

- It must be signed by the drawer.

- The drawer, drawee, and payee must be certain.

- The sum payable must also be certain.

- It should be properly stamped.

- It must contain an express order to pay money and money alone.

Cheques

Section 6 of the Act defines “A cheque is a bill of exchange drawn on a specified banker, and not expressed to be payable otherwise than on demand”. A cheque is a bill of exchange with two more qualifications, namely, (i) it is always drawn on a specified banker, and (ii) it is always payable on demand.

Consequently, all cheques are bills of exchange, but all bills are not cheques. A cheque must satisfy all the requirements of a bill of exchange; that is, it must be signed by the drawer and must contain an unconditional order on a specified banker to pay a certain sum of money to or to the order of a certain person or to the bearer of the cheque. It does not require acceptance.

Hundis

A “Hundi” is a negotiable instrument written in an oriental language. The term hundi includes all indigenous negotiable instruments whether they be in the form of notes or bills. The word ‘hundi’ is said to be derived from the Sanskrit word ‘hundi’, which means “to collect”.

They are quite popular among Indian merchants from the very old days. They are used to finance trade and commerce and provide a facile and sound medium of currency and credit. Hundis are governed by the custom and usage of the locality in which they are intended to be used and not by the provision of the Negotiable Instruments Act.

In case there is no customary rule known to a certain point, the court may apply the provisions of the Negotiable Instruments Act. It is also open to the parties to expressly exclude the applicability of any custom relating to hundis by agreement (under Chandra vs. Lachhmi Bibi, 7 B.I.R. 682).

Difference Between Bills of Exchange and Cheques

The following is the difference between bills of exchange and cheques:

- A bill of exchange is usually drawn on some person or firm, while a cheque is always drawn on a bank.

- It is essential that a bill of exchange must be accepted before its payment can be claimed A cheque does not require any such acceptance.

- A cheque can only be drawn payable on demand, a bill may be also drawn payable on demand, or on the expiry of a certain period after the date or sight.

- A grace of three days is allowed in the case of time bills while no grace is given in the case of a cheque.

- The drawer of the bill is discharged from his liability if it is not presented for payment, but the drawer of a cheque is discharged only if he suffers any damage by delay in presenting the cheque for payment.

- Notice of dishonor of a bill is necessary, but no such notice is necessary in the case of the cheque.

- A cheque may be crossed, but not needed in the case of a bill.

- A bill of exchange must be properly stamped, while a cheque does not require any stamp.

- A cheque drawn to the bearer payable on demand shall be valid but a bill payable on demand can never be drawn to the bearer.

- Unlike cheques, the payment of a bill cannot be countermanded by the drawer.

Parties to Negotiable Instruments

Parties to Bill of Exchange

-

Drawer: The maker of a bill of exchange is called the ‘drawer’.

-

Drawee: The person directed to pay the money by the drawer is called the ‘drawee’.

-

Acceptor: After a drawee of a bill has signed his assent upon the bill, or if there are more parts than one, upon one of such, pares and delivered the same, or given notice of such signing to the holder or to some person on his behalf, he is called the ‘ acceptor’.

-

Payee: The person named in the instrument, to whom or to whose order the money is directed to be paid by the instrument is called the ‘payee’. He is the real beneficiary under the instrument. Where he signs his name and makes the instrument payable to some other person, that other person does not become the payee.

-

Indorser: When the holder transfers or indorses the instrument to anyone else, the holder becomes the ‘indorser’.

-

Indorsee: The person to whom the bill is indorsed is called an ‘indorsee’.

-

Holder: A person who is legally entitled to the possession of the negotiable instrument in his own name and to receive the amount thereof, is called a ‘holder’. He is either the original payee or the indorsee. In case the bill is payable to the bearer, the person in possession of the negotiable instrument is called the ‘holder’.

-

Drawee in case of need: When in the bill or in any indorsement, the name of any person is given, in addition to the drawee, to be resorted to in case of need, such a person is called ‘drawee in case of need’. In such a case it is obligatory on the part of the holder to present the bill to such a drawee in case the original drawee refuses to accept the bill. The bill is taken to be dishonored by non-acceptance or for nonpayment, only when such a drawee refuses to accept or pay the bill.

- Acceptor for honor: In case the original drawee refuses to accept the bill or to furnish better security when demanded by the notary, any person who is not liable for the bill, may accept it with the consent of the holder, for the honor of any party liable on the bill. Such an acceptor is called an ‘acceptor for honor’.

Parties to a Promissory Note

- Maker. He is the person who promises to pay the amount stated in the note. He is the debtor.

- Payee. He is the person to whom the amount is payable i.e. the creditor. 3. Holder. He is the payee or the person to whom the note might have been indorsed.

- The indorser and indorsee (the same as in the case of a bill).

Parties to a Cheque

- Drawer. He is the person who draws the cheque, i.e., the depositor of money in the bank.

- Drawee. It is the drawer’s banker on whom the cheque has been drawn.

- Payee. He is the person who is entitled to receive the payment of the cheque.

- The holder, indorser, and indorsee (the same as in the case of a bill or note).

Negotiation

Negotiation may be defined as the process by which a third party is constituted as the holder of the instrument so as to entitle him to the possession of the same and to receive the amount due thereon in his own name.

According to section 14 of the Act, ‘when a promissory note, bill of exchange or cheque is transferred to any person so as to constitute that person the holder thereof, the instrument is said to be negotiated.’ The main purpose and essence of negotiation is to make the transferee of a promissory note, a bill of exchange, or a cheque the holder thereof. Negotiation thus requires two conditions to be fulfilled, namely:

- There must be a transfer of the instrument to another person.

- The transfer must be made in such a manner as to constitute the transferee the holder of the instrument.

Handing over a negotiable instrument to a servant for safe custody is not negotiation; there must be a transfer with the intention to pass the title.

Modes of Negotiation

Negotiation may be effected in the following two ways:

-

Negotiation by delivery (Sec. 47): Where a promissory note or a bill of exchange or a cheque is payable to a bearer, it may be negotiated by delivery thereof. Example: A, the holder of a negotiable instrument payable to the bearer, delivers it to B’s agent to keep it for B. The instrument has been negotiated.

- Negotiation by endorsement and delivery (Sec. 48): A promissory note, a cheque, or a bill of exchange payable to an order can be negotiated only by endorsement and delivery. Unless the holder signs his endorsement on the instrument and delivers it, the transferee does not become a holder. If there are more payees than one, all must endorse it.

FAQs About the Negotiable Instruments Act 1881

What is Negotiable Instruments?

A negotiable instrument is one, the property which is acquired by anyone who takes it bonafide and for value notwithstanding any defects of the title in the person from whom he took it.

What are the characteristics of negotiable instruments?

The following are the characteristics of negotiable instruments: Property 2. Title 3. Rights 4. Presumptions 6. Prompt Payment.

What is the presumption of negotiable instruments?

The presumption of negotiable instruments are: Consideration 2. Date 3. Time of Acceptance 4. Time of Transfer 5. Order of Indorsement 6. Stamp 7. Holder in Due Course 8. Proof of Protest.

What are the types of negotiable instruments?

These are the four types of negotiable instruments: Promissory Notes 2. Bill of Exchange 3. Cheques 4. Hundis.