Table of Contents

What is Supply?

Supply is the total quantity of a commodity that a seller would be willing to produce and sell at a given price, during a given period of time. However, we should understand the difference between ‘stock’ and ‘supply’. Stock is the quantity of a particular commodity in possession of a specific supplier at a point in time. It is not necessary that the quantity possessed by the producer will be available to be supplied at a price.

Table of Contents

The stock, of course, serves as a basis for supply. For example, a producer has 100 quintals of sugar in stock but he offers only 50 quintals of sugar at a time say for Rs. 15 per kg. He can increase the quantity to be offered in the market at a higher price.

The quantitative difference between ‘stock’ and ‘supply’ depends upon the price of the commodity, time period and also on the nature of the commodity.

Definitions of Supply

These are definitions of supply given by some economists:

[su_quote cite=”Lipsey”]Supply is a flow; it is so much per day, month or year.”According to Benham “Supply is the amount offered for sale per unit of time.[/su_quote]

[su_quote cite=”Meyers”]Supply may be defined as a schedule of the amount of a product that would be offered for sale at all possible prices at any one instant of time, or during any one period of time, for example, a day, a week, a month, a year and so on, in which the conditions of supply remain the same.[/su_quote]

[su_quote cite=”McConnell”]Supply may be defined as a schedule that shows the various amounts of a product which a particular seller is willing and able to produce and make available for sale in the market at each specific price in a set of possible prices during a given period.[/su_quote]

[su_quote cite=”Anatol Murad”]Supply refers to the quantity of a commodity offered for sale at a given price, in a given market, at a given time.[/su_quote]

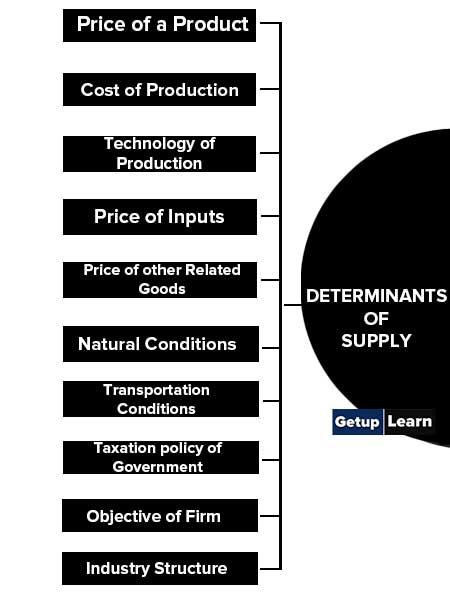

Determinants of Supply

The supply of a commodity also depends on the technology used in the production of the commodity and many other factors. The main factors determinants of supply of a commodity are:

- Price of a Product

- Cost of Production

- Technology of Production

- Price of Inputs

- Price of other Related Goods

- Natural Conditions

- Transportation Conditions

- Taxation policy of Government

- Objective of Firm

- Industry Structure

Price of a Product

The major determinant of the supply of a product is its price. An increase in the price of a product increases its supply and vice versa while other factors remain the same. Producers increase the supply of the product at higher prices due to the expectation of receiving increased profits. Thus, price and supply have a direct relationship.

Cost of Production

It is the cost incurred on the manufacturing of goods that are to be offered to consumers. Cost of production and supply are inversely proportional to each other. This implies that suppliers do not supply products in the market when the cost of manufacturing is more than their market price.

In this case, sellers would wait for a rise in price in the future. The cost of production increases due to several factors, such as loss of fertility of the land; high wage rates of labour; and increase in the prices of raw materials, transportation costs, and tax rate.

Technology of Production

An improvement in the technology of production of a commodity decreases the per-unit cost of the commodity. The margin of profit will increase at the same price. So the supply of a commodity will increase, with improvement in technology of production, at the same price.

On the other hand, if a firm uses absolute technology of production, the cost of production per unit of the commodity will increase. The margin of profit will decrease, so the firm will decrease its supply at the same price. This is the main reason that the firms are trying to use better technology of production because it not only reduces the cost of production per unit but also improves the quality of the product.

Price of Inputs

Suppose a firm is producing ice cream. If the price of milk falls, the cost of production per unit of ice creams will fall. It will lead to an increase in the margin of profit per unit. So, the firm will increase the supply of ice cream. On the other hand, if the price of milk increases, the cost of production per unit of ice cream will increase.

It will lead to a decrease in the margin of profit and the firm will decrease the supply of ice cream. Thus, if the price of any input used in the production of a commodity falls, it leads to a decrease in the cost of the production per unit and as a result supply of the commodity will increase.

On the other hand, an increase in the price of any input used in the production of a commodity increases the cost of production per unit and decreases the supply of the commodity.

The supply of a commodity is also influenced by the price of other related goods. Let us suppose that a farmer produces two goods wheat and rice with the help of given resources. If the price of rice increases, it will be more profitable for the farmer to produce more rice.

The farmer will divert his resources from the production of wheat to the production of rice. As a result, the supply of rice will increase and that of wheat will decrease. On the other hand, a fall in the price of rice will result in a decrease in the supply of rice and an increase in the supply of wheat.

Natural Conditions

The supply of certain products is directly influenced by climatic conditions. For instance, the supply of agricultural products increases when the monsoon comes well on time. On the contrary, the supply of these products decreases at the time of drought. Some of the crops are climate-specific and their growth purely depends on climatic conditions.

For example, Kharif crops are well grown at the time of summer, while Rabi crops are produced well in the winter season.

Transportation Conditions

Better transport facilities result in an increase in the supply of goods. Transport is always a constraint to the supply of goods. This is because goods are not available on time due to poor transport facilities. Therefore, even if the price of a product increases, the supply would not increase.

Taxation policy of Government

If the government reduces the excise duty or the production of a commodity, the cost of production per unit of the commodity will decrease, and the margin of profit will increase at the same price so the producer of the commodity will increase its supply.

It happens when the government wants to increase the production of the commodity. On the other hand, to discourage the production of some harmful goods, like cigarettes, liquor etc, the government increases the rate of excise duty on the production of such goods. So the cost of production per unit of the commodity increases and the supply of such commodities decreases.

Objective of Firm

The objective of the producer also influences the supply of a commodity. Generally, the objective of a producer is getting maximize his profits. Profits are maximized at a higher price. So he increases the supply of a commodity at a higher price and decreases its supply at a lower price.

But sometimes, the producer may be in maximizing his sales and not maximizing his profits as he wants to capture the market. In that case, he goes on increasing the supply so long his target is not achieved can profit is not adversely affected. He may increase the supply at the same price to any extent.

Industry Structure

The supply of goods is also dependent on the structure of the industry in which a firm is operating. If there is a monopoly in the industry, the manufacturer may restrict the supply of his/her goods with an aim to raise the prices of goods and increase profits.

On the other hand, in the case of a perfectly competitive market structure, there would be a large number of sellers in the market. Consequently, the supply of a product would increase.

Law of Supply

The Law of supply explains the relationship between the price of a commodity and its quantity supplied. Other things remain the same when the price of a commodity falls the quantity supplied decreases and vice versa. Thus there is a positive relationship between the price of a commodity and its supply.

One thing that should be understood here is that the law of supply is only an indicative statement, not a quantitative statement. It means that when the price will change the quantity supplied will also change in the direction of price change but will not explain ‘how much.

For example, if the price of a commodity increases by 10% the quantity supplied, as per the law of supply, will also increase thus, the law of supply states a direct relationship between the price of a product and its supply. Therefore, both price and supply move in the same direction.

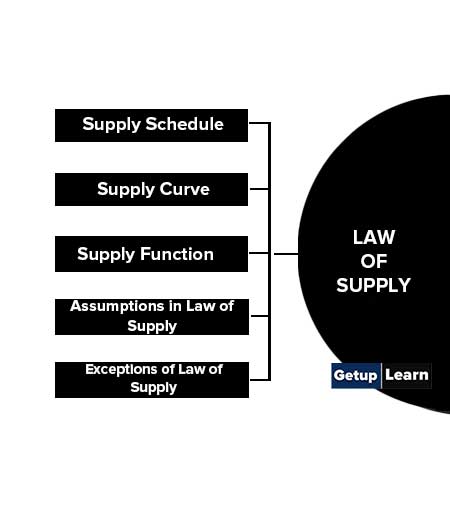

To understand the law of supply, it is important to discuss the concepts of demand schedule and demand curve:

- Supply Schedule

- Supply Curve

- Supply Function

- Assumptions in Law of Supply

- Exceptions of Law of Supply

Supply Schedule

A supply schedule can be defined as a tabular representation of the law of supply. It represents the quantities of a product supplied by a supplier at different prices and time periods, keeping all other factors constant. There can be two types of supply schedules, namely individual supply schedules and market supply schedules.

These two types of supply schedules are explained as follows:

Individual Supply Schedule

This schedule represents the quantities of a product supplied by an individual firm or supplier at different prices during a specific period of time, assuming other factors remain unchanged. Let us understand the individual supply schedule with the help of an example. The table shows the supply schedule of a firm supplying commodity A:

Individual Supply Schedule for Commodity A

| Price of the Product (₹per Kg) | Quantity Supplied of Commodity A (Kg per Week) |

| 5 | 3,000 |

| 10 | 8,000 |

| 15 | 12,000 |

| 20 | 15,000 |

From Table 3.1, it is clear that the firm is supplying 3,000 kg per week of commodity A at the price of ₹5 per kg. As the price rises from ₹5 to ₹10, the firm also increased the supply to 8,000 per kg. Therefore, the individual supply schedule shown in the Table indicates that the quantity supplied increases with a rise in price.

Market Supply Schedule

This schedule represents the quantities of a product supplied by all firms or suppliers in the market at different prices during a specific period of time, while other factors are constant. In other words, the market supply schedule can be defined as the summation of all individual supply schedules. The table shows the market supply schedule of two firms X and Y for commodity A:

Market Supply Schedule for Commodity A

| Price of Product A (₹ per kg) | Quantity Supplied by Firm X (1000 kg per week) | Quantity Supplied by Firm Y (1000 kg per week) | Market Supply (1000 kg per week) |

| 5 | 3 | 7 | 10 |

| 10 | 8 | 12 | 20 |

| 15 | 12 | 15 | 27 |

| 20 | 15 | 17 | 32 |

In Table 3.2, market supply is calculated by combining the quantities supplied by firms X and Y. It also shows when the commodity is priced at ₹5per kg, the market supply of commodity A is 10,000 kg per week. When the price rises to ₹10 per kg, the market supply also increases to 20,000 per kg. So it can be observed, that a rise in the price of commodity A increases the market supply.

Supply Curve

The graphical representation of the supply schedule is called the supply curve. In a graph, the price of a product is represented on Y-axis and the quantity supplied is represented on X-axis. The supply curve can be of two types, individual supply curve and market supply curve. These two types of supply curves are explained as follows:

Individual Supply Curve

It is the graphical representation of individual supply schedules. The individual supply schedule of commodity A represented in Table when plotted on a graph will provide the individual supply curve, which is shown in Figure.

The slope moving upwards to the right in the individual supply curve shows the direct relationship between supply and price, i.e. increase in supply along with the rise in prices.

Market Supply Curve

It is the graphical representation of the market supply schedule. The market supply schedule of commodity A (supplied by Firm X and Firm Y) is represented in Table, when plotted on the graph will provide the market supply curve, which is shown in Figure.

Supply Function

The supply function is the mathematical expression of the law of supply. In other words, the supply function quantifies the relationship between the quantity supplied and the price of a product, while keeping the other factors constant. The law of supply expresses the nature of the relationship between quantity supplied and the price of a product, while the supply function measures that relationship.

The supply function can be expressed as:

Qs = f (Pa, Pb, Pc, T, Tp)

Where,

- Qs = Supply

- Pa = Price of Good Supplied

- Pb = Price of Other Goods

- Pc = Price of Factor Input

- T = Technology

- Tp = Time Period

According to the supply function, the quantity supplied of a good (Qs ) varies with the price of that good (Pa ), the price of other goods (Pb), the price of factor input (Pc ), the technology used for production (T), and time period (Tp).

Assumptions in Law of Supply

All the factors other than the price are assumed to be constant. The law of supply works on certain assumptions which are given as follows:

- The income of buyers and sellers remains unchanged.

- The commodity is measurable and available in small units.

- The tastes and preferences of buyers remain unchanged.

- The cost of all factors of production does not change over a period of time.

- The time period under consideration is short.

- The technology used remains constant.

- The producer is rational.

- Natural factors remain stable.

- Expectations of producers and government policy do not change over a period of time.

Exceptions of Law of Supply

Some important exceptions of law of supply are:

Agricultural Products

The law of exception is not applicable to agricultural products. The production of these products is dependent on so many factors which are uncontrollable, such as climate and availability of fertile land. Thus, the production of agricultural products cannot be increased beyond a limit. Therefore, even a rise in price cannot increase the supply of these products beyond a limit.

Goods for Auction

Auctions goods are offered for sale through bidding. The auction can take place due to various reasons, for instance, a bank may auction the assets of a customer in case of his failure in paying off the debts over a period of time. Thus, the supply of these goods cannot increase or decrease beyond a limit. In the case of these goods, a rise or fall in price does not impact the supply.

Expectation of Change in Prices in Future

The Law of supply is not applicable under the circumstances when there is an expectation of change in the prices of a product in the near future. For instance, if the price of wheat rises and is expected to increase further in the next few months, sellers may not increase supply and store huge quantities in the hope of achieving profits at the time of a price rise.

Supply of Labour

The law of supply fails in the case of labour. After a certain point, the rise in wages does not increase the supply of labour. At higher wages, labour prefers to work for lesser hours. This happens due to a change in preference of labour for leisure hours.

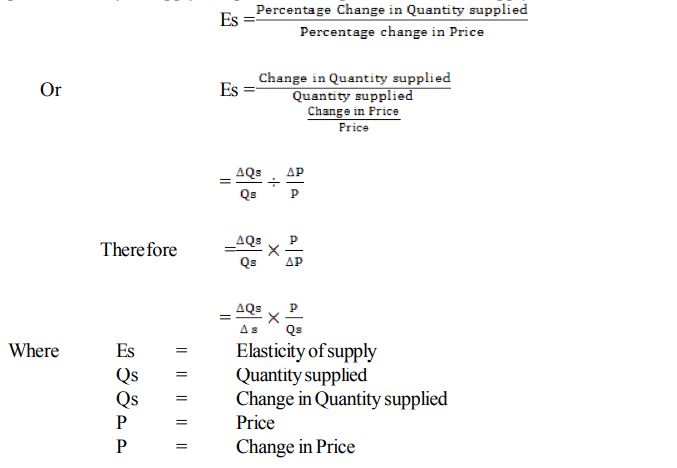

Elasticity of Supply

The elasticity of supply expresses the degree of responsiveness of the supply for a commodity to a change in its price. It is the ratio of percentage change in quantity supplied to the percentage change in price. The elasticity of supply is a quantitative expression of the law of Supply.

There is a direct and positive relationship between quantity supplied and price. The supply curve slopes positively from left to right.

Degrees of Elasticity of Supply

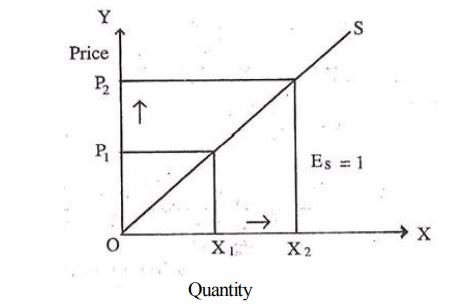

Unitary Elasticity of Supply (Es = 1)

When a proportionate change in price causes an equal and proportionate change in quantity supplied, supply is said to be unitary elastic. In such a case the supply curve shall pass through the origin. When the price for good X, rises from OP1 to OP2, as shown in diagram 1, the quantity supplied extends proportionately from OX1 to OX2. A rise in price leads to a proportionate extension in supply.

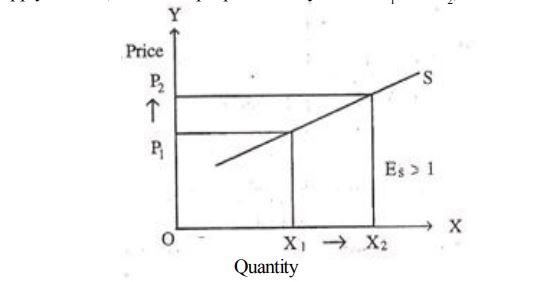

Relatively Elastic Supply (Es> 1)

When a proportionate change in price causes a more than proportionate change in supply, supply is said to be relatively elastic. As the price rises from OP1 to OP2, the supply extends, more than proportionately from OX1 to OX2, as shown in diagram 2.

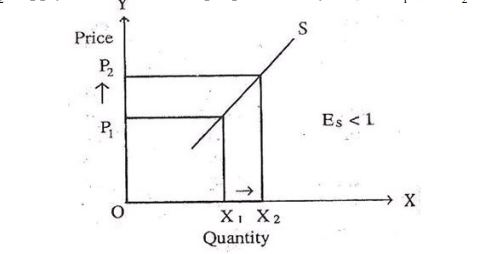

Relatively Inelastic Supply (Es <1)

When a proportionate change in Price causes a less than proportionate change in supply, supply is said to be relatively inelastic. When the price increases from OP1 to OP2, supply extends less than proportionately from OX1 to OX2. This is shown in diagram 3.

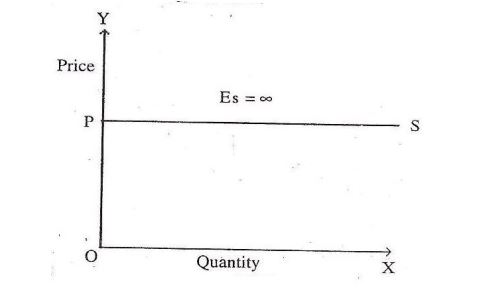

Perfectly Elastic Supply

When an infinite rise in prices leads to an infinitely large extension in quantity supplied, the elasticity of supply is perfectly elastic. The perfectly elastic supply curve is a horizontal straight line, parallel to the X-axis, showing quantity supplied at a height of the price. This is shown in diagram 4.

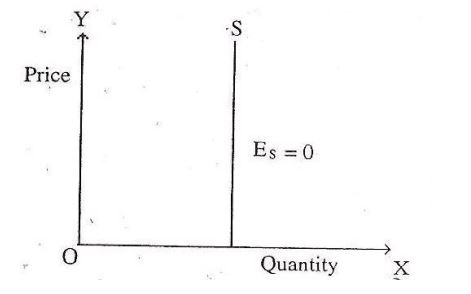

Perfectly Inelastic Supply

Supply is said to be perfectly inelastic when, howsoever, much price may rise or fall, the quantity supplied remains the same. The perfectly inelastic supply curve, as shown in diagram 5, is a straight vertical line perpendicular to the X-axis and parallel to the Y-axis.

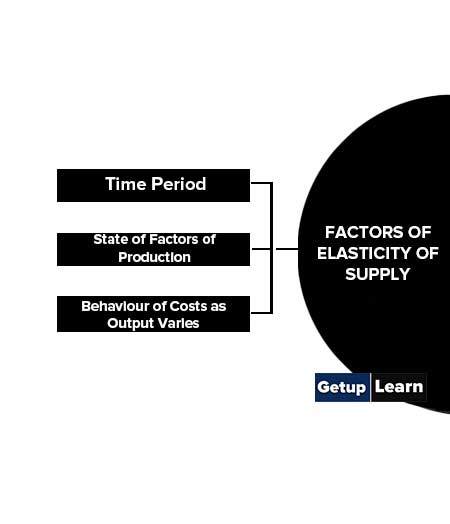

Factors of Elasticity of Supply

The elasticity of supply is determined by the following factors:

Time Period

The elasticity of supply depends upon the time that the seller requires to bring about an adjustment in supply. In the very short period where the supply of commodities is limited to the existing stocks, the supply is perfectly inelastic.

In the short period, the supply of the commodity can be changed by altering the variable factors of production by having additional shifts or by using the existing plant and machinery more intensively. In the long period, the supply has enough time to adjust itself to changes in demand. It is a time period in which all factors become variable. The elasticity of supply in the long period will be highly elastic.

State of Factors of Production

The supply of a commodity depends upon production factors. To increase production the seller will have to employ more units of the factors of production. If factors of production are scarce, they will have to be paid a higher price for the production of that particular commodity.

The supply curve in such a case shall be less elastic. If the factors of production are available abundantly, the cost of employing such factors will be less and, therefore, the supply will be more elastic.

Behaviour of Costs as Output Varies

If the cost of production rise rapidly as the output rises, then the incentive to expand production in response to price rise will be limited due to an increase in costs. In this case, the supply will be inelastic. On the other hand, if the cost of production rises slowly as output increases, a rise in price that raises profits will bring forth a large increase in quantity supplied. In this case, the supply will be more elastic.

What do you mean supply?

Supply is the quantity of a particular commodity that a producer is willing to produce and sell in the market at a price at a time.

What is stock?

Stock is the quantity of a particular commodity in possession of a specific supplier at a point of time.

What is Elasticity of supply?

The elasticity of supply is the degree of responsiveness of the supply for a commodity to the percentage change in price.

What are the 7 determinants of supply?

The main factors determinants of the supply of a commodity are (1) Price of a Product, (2) Cost of Production, (3) Technology of Production, (4) Price of Inputs, (5) Price of other Related Goods, (6) Natural Conditions, (7)Transportation Conditions etc.

What is supply in the law of supply?

The Law of supply explains the relationship between the price of a commodity and its quantity supplied. Other things remain the same, when the price of a commodity falls the quantity supplied decreases and vice versa. Thus there is a positive relationship between the price of a commodity and its supply.